Medicare Advantage Plans Protect High Profit Scams

Medicare Advantage is a cash cow for insurers, and they know how to milk the system: boost profits via overcharge schemes, block government regulation, and when push comes to shove, abandon costly insurance markets.

October 10, 2024

Health Insurer Financial Performance in 2023

KFF

Jared Ortaliza et al.

July 2, 2024

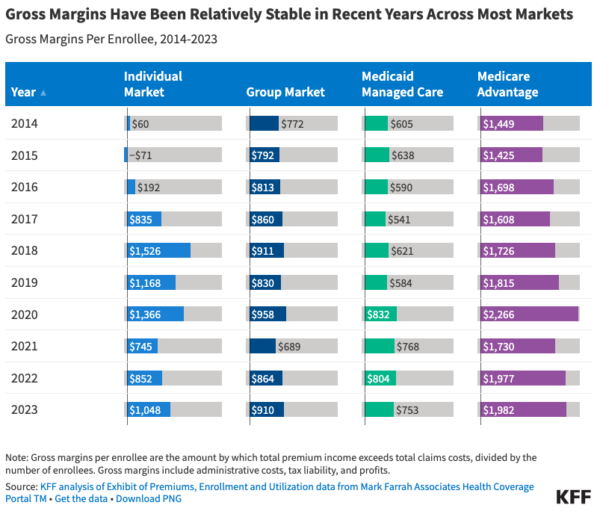

At the end of 2023, gross margins per enrollee ranged from $753 in the Medicaid managed care market to $1,982 in the Medicare Advantage market. Gross margins [amount by which premiums exceed claims costs] per enrollee in the group and individual markets were $910 and $1,048, respectively, roughly half the level observed among Medicare Advantage plans on average.

The Medicare Advantage Influence Machine

KFF News

September 30, 2024

By Fred Schulte and Holly K. Hacker

Federal officials resolved more than a decade ago to crack down on whopping government overpayments to private Medicare Advantage health insurance plans, which were siphoning off billions of tax dollars every year.

But Centers for Medicare & Medicaid Services officials have yet to demand any refunds — and over the years the private insurance plans have morphed into a politically potent juggernaut that has signed up more than 33 million seniors and is aggressively lobbying to stave off cuts.

Critics have watched with alarm as the industry has managed to deflate or deflect financial penalties and steadily gain clout in Washington through political contributions; television advertising, including a 2023 Super Bowl feature; and other activities, including mobilizing seniors. …

David Lipschutz, an attorney with the Center for Medicare Advocacy, a nonprofit public interest law firm, said policymakers have an unsettling history of yielding to industry pressure. “The health plans throw a temper tantrum and then CMS will back off,” he said. …

CMS, the Baltimore-based agency that oversees Medicare, has long felt the sting of industry pressure to slow or otherwise stymie audits and other steps to reduce and recover overpayments. These issues often attract little public notice, even though they can put billions of tax dollars at risk.

In August, KFF Health News reported how CMS officials backed off a 2014 plan to discourage the health plans from overcharging amid an industry “uproar.” The rule would have required that insurers, when combing patients’ medical records to identify underpayments, also look for overcharges. Health plans have been paid billions of dollars through the data mining, known as “chart reviews,” according to the government.

CMS efforts to tighten oversight stalled amid years of technical protests from the industry — such as arguing that audits to uncover overpayments were flawed and unfair.

Revolving Door

At least a dozen witnesses in the UnitedHealth case and a similar DOJ civil fraud case pending against Anthem are former ranking CMS officials who departed for jobs tied to the Medicare Advantage industry.

Marilyn Tavenner is one. She led the agency in 2014 when it backed off the overpayment regulation. She left in 2015 to head industry trade group AHIP, where she made more than $4.5 million during three years at the helm, according to Internal Revenue Service filings.

And in October 2015, as CMS department chiefs were batting around ideas to crack down on billing abuses, including reinstating the 2014 regulation on data mining, the agency was led by Andy Slavitt, a former executive vice president of the Optum division of UnitedHealth Group. …

CMS came up with an audit program that selected 30 plans annually, taking a sample of 201 patients from each. Medical coders checked to make sure patient files properly documented health conditions for which the plans had billed.

In a May 2016 private briefing, CMS indicated that the health plans owed from $98 million to $163 million for 2011 depending on how the overpayment estimate was extrapolated, court records show.

But CMS still hasn’t collected any money. In a surprise action in late January 2023, CMS announced that it would settle for a fraction of the estimated overpayments and not impose major financial penalties until 2018 audits, which have yet to get underway. Exactly how much plans will end up paying back is unclear.

Insurers cut Medicare Advantage plans for 2025

Business Insurance

Oct 4, 2024

Major insurers, including Aetna and Humana, are cutting back on Medicare Advantage plans for 2025, potentially affecting policyholder costs and care arrangements for seniors, Axios reports. This reduction follows policy changes by the Biden administration, leading insurers to adjust offerings and exit some markets. While average premiums are set to decrease slightly, the number of available plans per county has dropped.

Comment by: Jim Kahn

Medicare Advantage is highly profitable, with gross margins of $2000 per patient, 2-3 times higher than other health insurance sectors. Year after year.

The profitability derives from overcharging, via inflated diagnostic coding and risk selection, among other tactics. The overcharge exceeds $100 billion per year.

Further, these numbers understate real profits, because insurers overpay their proliferating affiliated companies (such as PBMs) in a ballooning corporate structure. It’s a shell game, designed to keep within “medical loss ratio” limits. The process is well described by HEALTH CARE un-Covered.

The regulators – CMS (Center for Medicare and Medicaid Services) – understand these problems. But heavy lobbying and a revolving door between CMS and insurers suppresses regulatory action. In the example above, in 2023 a penalty for overcharges prior to 2011 was sharply reduced, because the plans insisted that the findings couldn’t be extrapolated to all beneficiaries. The next step was postponed pending completion of audits from 2018, 5 years earlier! Why so slow? I suspect insurer foot-dragging. The insurers will fight those findings too.

When CMS does manage to scale back overpayment, as they’ve done to small degree in setting premium growth rates for 2025, the insurer response is to assure investors that they can cut costs, and to exit expensive (money-losing) markets (above and here). Who suffers? Sicker than average Medicare enrollees, and traditional Medicare.

Paying for health care shouldn’t be about private insurer profits, overcharges, lobbying, and market maneuvering. It should be about efficiently meeting the health care needs of the population.

About the Commentator, Jim Kahn

Jim (James G.) Kahn, MD, MPH (editor) is an Emeritus Professor of Health Policy, Epidemiology, and Global Health at the University of California, San Francisco. His work focuses on the cost and effectiveness of prevention and treatment interventions in low and middle income countries, and on single payer economics in the U.S. He has studied, advocated, and educated on single payer since the 1994 campaign for Prop 186 in California, including two years as chair of Physicians for a National Health Program California.

See All PostsYou might also be interested in...

Recent and Related Posts

Premier Medical Journal Scrutinizes Corporatization of US Health Care

Laying out the Ill-Effects of Medicaid Cuts in the Congressional Budget Bill